Precision

Timely and accurate payout deliveries.

20K +

used this app

Our trustees & partners.

Whether you're saving for a dream, a necessity, or an investment, Mipango Mchezo helps you achieve goals like:

Timely and accurate payout deliveries.

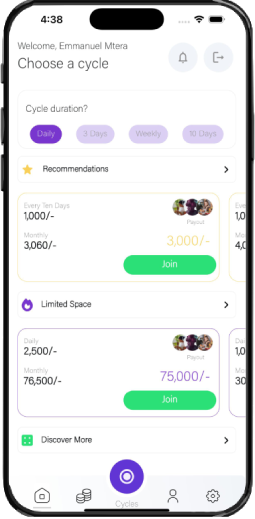

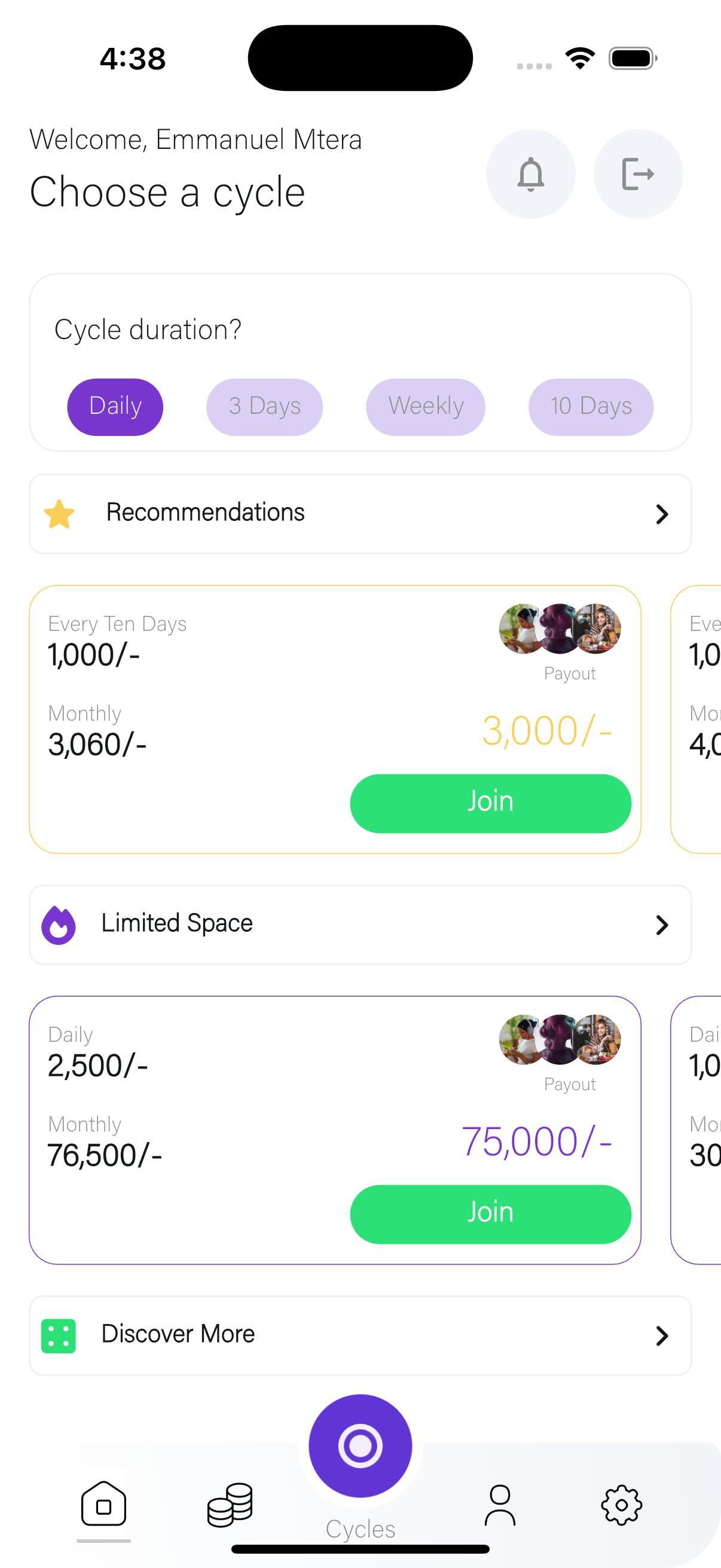

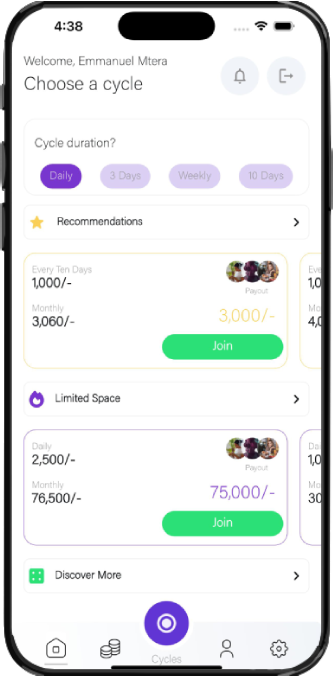

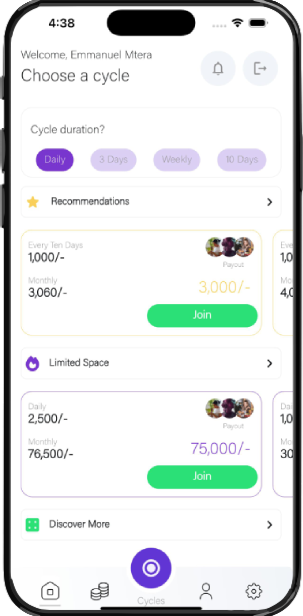

Contribute what fits your budget—starting as low as TZS 1,000 daily up to TZS 500,000. Advance contributions are welcome.

Even if members face payment challenges, Mipango ensures your payouts remain unaffected.

Your savings are safeguarded, hosted securely by CRDB Bank. Even in challenging situations, we've got you covered.

Mipango Mchezo is designed to meet the principles of Islamic Sharia. Approved by certified Sharia consultants, our system ensures compliance for all users.

Download the app on either Android or iOS and register using your mobile number. Complete OTP verification.

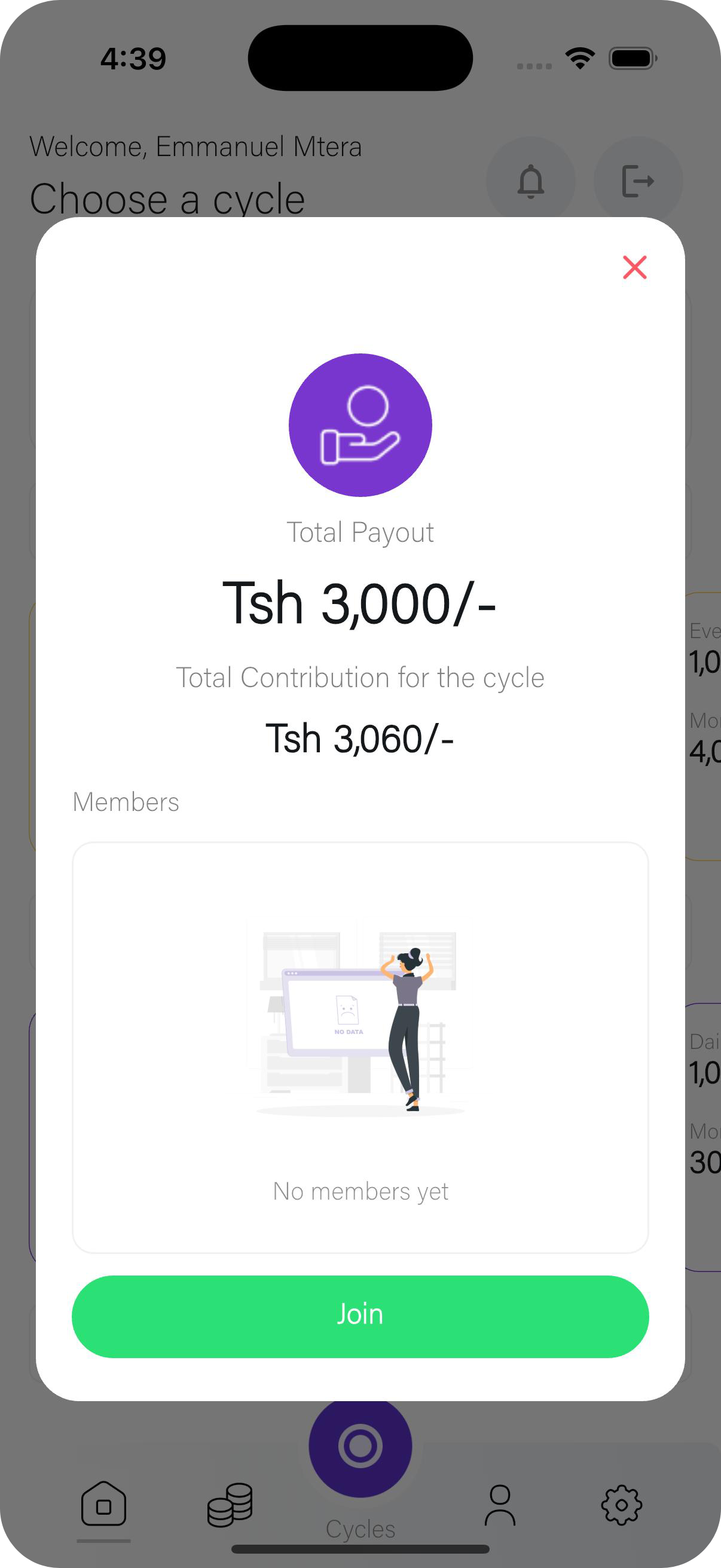

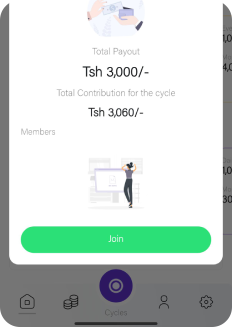

Explore saving cycles (mchezo)

- Filling in your NIDA number and completing NIDA verification.

- Adding 1-2 referees with their phone and NIDA numbers (OTP verification required).

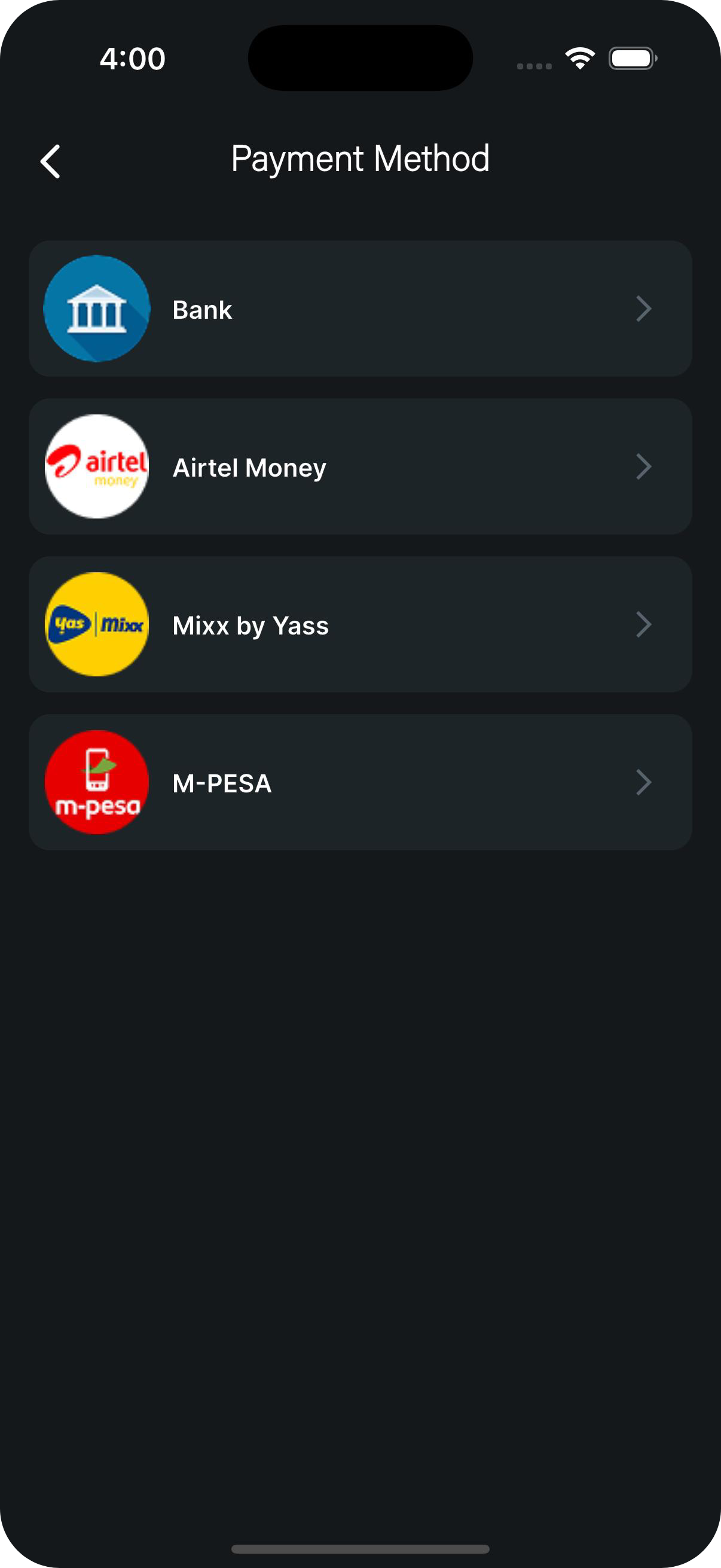

- Linking your payout account—mobile money or bank account.

- Pay contributions via mobile money, bank, or money agents.

- Receive your payout directly into your registered bank account on your payout date (minus penalties, if any).

Mipango Mchezo is a digitized merry-go-round that allows users to join saving circles, make contributions, and receive payouts to achieve their financial goals.

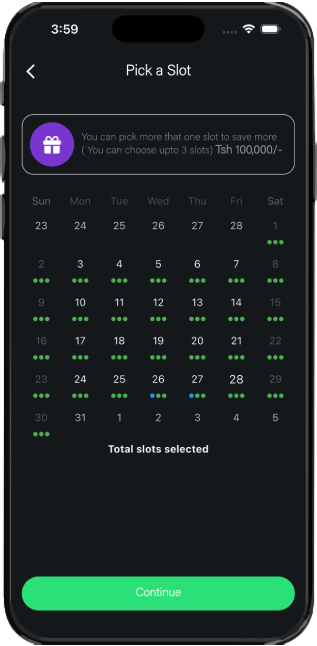

Yes, you can join multiple circles and even choose up to three slots per circle to maximize your savings and payouts.

Circles will start on time, regardless of whether all slots are assigned. Unallocated slots will automatically be filled by Mipango bots, and this will not affect the payout amounts.

Use the "Home" feature to browse various circle options and join as many as you like, depending on your goals and eligibility.

Instant free download from Apple Store and Google Playstore.